Exclusive 69th Update Coaching Sale (peep the details below)

SA 2026 interview szn is fast approaching! Don’t fall behind your competition by wasting time tracking applications.

For the next month, we will be running a 30% sale for the purchase of our Premium Database. Details of our Premium Database can be found below. Venmo @ThePulsePrep $35 or pay with credit card Premium Database 30% Sale ---Stripe.com and shoot us an e-mail @[email protected]

Video of Premium Database——>The Pulse Database Video

2 Coaching Sessions for only $69! This is a special, one-time offer for this week only to receive 2, one-hour coaching sessions for only $69. A coaching session is usually $50 / hour, so this is an absolute steal to get prepped for the summer 2026 recruiting season. (Venmo @ThePulsePrep or pay with credit card: ($69 for 2 Coaching Sessions). Interviews are right around the corner and we want you to be as prepared as possible. Last year, 95% of those coached received offers!

The Wall Street Rollup:

Introducing the Wall Street Rollup (Wall Street Rollup -- (beehiiv.com)

WSR is a 2x/week, finance, markets, and investing newsletter that you can digest in a few minutes.

The Wall Street Rollup was formed to deliver a high-quality aggregator of Earnings, Transactions, and Headline updates (I personally love the transactional content).

This is the Finance Newsletter that Students need to keep up to date with the industry.

Join the Free Newsletter read by 15,000 professionals from Investment Banks, Asset Managers, and more.

Recruiting Timeline:

Banking:

Where We’re At:

SA 2026: Only one bank, HL, has announced the release date of its application (check "The Pulse" --#64 (FIRST SA 2026 APP) / Turnover in Finance (beehiiv.com) for detail.

Coffee chats / information sessions are ramping up at select schools for select banks. These events SUCK. It’s like 8 students per one analyst / associate and you gain little unique information. However, showing face is part of the game + name-dropping a few people you met in your cover letter will pay dividends when you ultimately apply.

SA 2025: CRC-IB and Bourne Partners opened their applications this week. This process is 99% complete and we will stop tracking as summer 2026 volume picks up. The total bank number is at 128 for the SA 2025 season.

FT 2025: Capital One, CIBC, CRC-IB, and more opened their FT apps this week. There are currently 52 firms actively recruiting for FT 2025. Please reach out if you are looking for coaching!

New SA 2026 Applications:

None

New SA 2025 Applications:

Bourne Partners: Sponsor-backed M&A advisory (SA 2025)

CRC-IB: Energy boutique (SA 2025)

New FT 2025 Applications:

Capital One: Building out their IB practice (FT 2025)

BMO: Middle-market Canadian bank (FT 2025)

Credit Agricole: Large French bank, ABL analyst (FT 2025)

Standard Chartered Bank: Middle-market (FT 2025)

CIBC: Large Canadian bank (FT 2025)

CRC-IB: Energy boutique (FT 2025)

See below to gain access to our premium database, updated weekly, which houses the application processes for over 200+ banks/consulting/buyside firms! Gain an edge over everyone else by not having to spend countless hours tracking applications and deadlines.

Consulting:

Where We’re At:

Only one application was released this week. 45 SA 2025 applications have been released along with 47 FT 2025 apps. Application releases will taper off at the end of October.

*We updated the networking contacts in the premium database so take advantage of that resource.

SA 2025 released apps:

None

FT 2025 released apps:

Capco: Associate Program (tech/digital transformation)

Apply ASAP if you’re interested!

Buyside:

Where We’re At:

SA 2026: Stone Point announced its SA 2026 PE application. There are currently 3 buyside firms actively recruiting for summer 2026 positions across PE, Growth, and VC. Looks like the buyside is jumping the gun faster than the banks!

SA 2025: RockCreek and Trillium Trading opened their SA 2025 apps this week. This brings the total buyside count to ~148 opened applications.

New SA 2026 released apps:

Stone Point: Multi-asset alternative investment manager, PE intern (SA 2026)

New SA 2025 released apps:

RockCreek: Investment intern (SA 2025)

Trillium Trading: Equities trading (SA 2025)

Premium Database:

The database is updated weekly and contains 200+ Investment Banking and Consulting internships/full-time positions along with:

Interview tips for specific companies

Interview prep material

Applications and deadlines linked so that you can apply with one click

Insider information about the application process

Professionals to network with

Buyside deadlines, interview prep, and people to network with for the sweatiest of students

We send the updated dataset every week with the latest banking and consulting job postings. We released our 69th update today.

Students we have been helping have already landed roles at Blackstone, Goldman, J.P. Morgan, Jefferies, Citi, and Solomon.

To get access to the database and the weekly updates, you pay a one-time fee of $35 (Venmo: ThePulsePrep / Credit Card: (Premium Database 30% Sale ---Stripe.com) that grants you annual access to the updated database (You can enable purchase protection if concerned). If you don’t find our services helpful, we simply ask for feedback on an area we can improve upon and will refund your $35.

This is a small investment for a huge payout when you secure your dream offer!

Video of Premium Database——>The Pulse Database Video

Market Update:

50 States, 50bps of Rate Cuts - (Sorry for the long read, but worth it)

69th update and rate cuts in the same week? Holy shit, this is perfect.

On Wednesday, the FED cut rates by 50bps from 5.25 - 5.50% to 4.75% - 5.00%. Rates haven’t moved since July of 2023 and haven’t been cut since before March 2022.

Recent Rate History (Source: Forbes)

Everyone has been waiting for this. With inflation around 2.5% and unemployment at 4.2%, the FED needed to begin cutting rates to avoid unemployment creeping to dangerous levels.

These cuts will spur demand. Demand for goods, demand for debt, and demand for deal flow ("The Pulse" --#32).

What will change?:

From a holistic lens:

In recent history, the FED has entered quantitative easing 12 separate times. Of those 12 times, 8 led to a recession and 4 led to a soft landing. The narrative here is that the FED is reactionary and typically cuts too late (i.e. the economic cracks have already widened).

Also, fundamentals would point out that the $USD should experience some devaluation ("The Pulse" --#55 / Rate Cut Imbalances and "The Pulse" --#22)

I can go into an entire write-up on these statements alone, but I will save that for another week.

From a corporate lens:

Rate cuts = cheaper debt. Corporations have a mix of floating and fixed-rate debt. Thankfully, much of the fixed rate debt was issued in the ZIRP era when benchmark rates were near 0%. With rate cuts, many corporations will experience a natural financial tailwind as their interest expense is reduced on floating-rate debt products. Less interest expense = more cash flow = better stock performance.

This contributes to a short-term, positive bounce in equities as experienced over the last two trading sessions (S&P 500 +1.4% and NASDAQ +2.1%).

Cheaper debt will also lead to greater debt issuance. The debt markets have been firing on all cylinders since the start of 2024 as spreads compressed to record tight levels ("The Pulse" --#40)

Tight spreads + a lower benchmark = more debt issuance. Corporations will flock to issue cheaper debt and investors will flock to buy this debt since the benchmark is still relatively high at > 4%.

From a consumer lens:

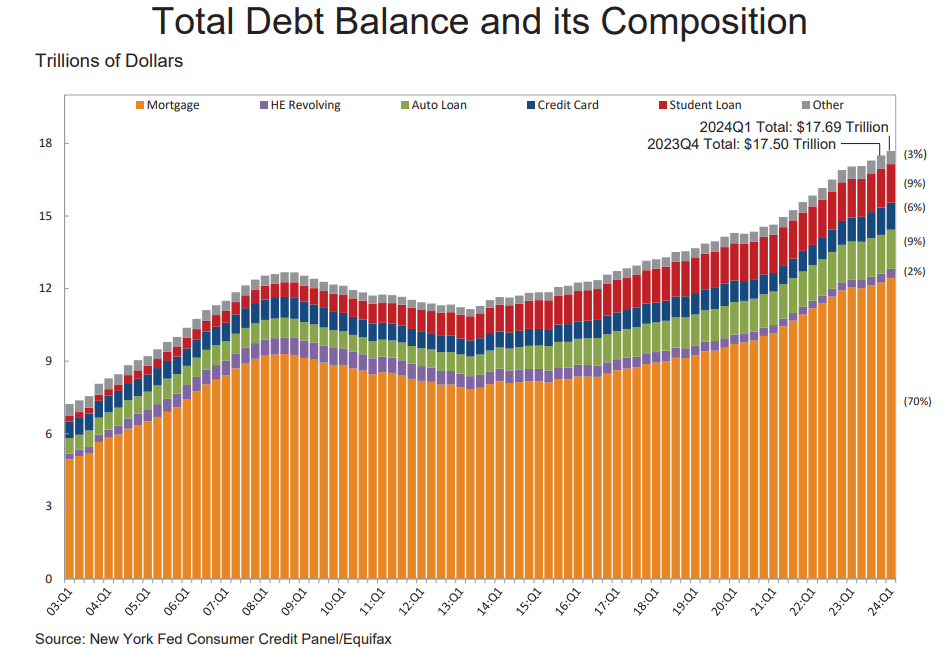

The bulk of consumer debt is tied up in fixed-rate products (mortgages, auto loans, etc) originated in the ZIRP era.

80-90% of Consumer Debt is Fixed

Long gone are the days of swinging adjustable-rate mortgages (ARMs). 95% of Americans have a 30-year, fixed rate mortgage and 60% of those have rates locked in below 4%. Therefore, most Americans are content with their low-rate mortgages and an immediate change in rates won’t impact them.

As you can see in the chart, only ~8-10% of consumer debt is floating (HELOCs and Credit Cards).

Everyone has a credit card, but only ~10% of credit card users are delinquent. As you know, you don’t get charged interest on your credit card balance unless you’re delinquent. So, only those delinquent borrowers will feel any type of immediate relief on their credit card interest expense.

What I’m getting at is that consumers are not immediately experiencing any significant reprieve in interest expense due to rate cuts since the bulk of their debt is fixed. The 50bps rate cut on Wednesday, doesn’t make a consumer’s life different from a debt perspective.

However, the story gets interesting from an asset perspective.

~25% of Assets Tied Up In Floating-Rate Products

Deposits, debt securities, and likely some of the assets baked into the ‘other’ category are all floating-rate products used by consumers to generate income. As rates are cut, the yields on these products are reduced.

A reduction in the yield on floating-rate assets paired with the consistency of the yield on fixed-rate debt = less income. Rate cuts today, have a negative effect on the income spread between consumer assets and liabilities. Also, wage growth is declining. Currently hovering around 4.6%.

No matter how you chop it up, a reduction in the asset-liability consumer income spread and a reduction in wage growth means consumers will experience less cash in the door every month unless inflation is materially suppressed.

Other asset values like homes and equities may increase, but that’s just paper gains. Not cash.

Where do we go?:

Rates are certainly going to be cut further. The big guessing game is deciding where they will end up. What’s the long-term federal funds rate?

Material softening of the economy will lead to greater cuts at a faster cadence. Economic resilience will lead to fewer cuts at a slower cadence. The FED remains data-dependent. You can be certain that the next few PCE and unemployment readings will heavily dictate the course of quantitative easing.

What’s our guess?

In December of 2023, we stated there will be ~75-100bps of cuts in 2024. Right now, that seems like a winning view (in March some mfers were saying 6 cuts and we got a little shaky on our view lol).

This FED has stuck to their word time and time again over the last few years, so we are siding close to the dots.

The FED’s dot-plot points to rates settling between 300 and 375bps by the end of 2025:

Source: Investopedia

That number seems reasonable, ~200bps of cuts. The ‘smart money’ (fixed-income investors) view rates settling around 275bps. That seems a touch South.

Our view is that rates will settle around 300 - 350bps by the end of 2025 which is ~150 - 200bps of additional cuts over the next 15 months. The average cutting cycle in recent history is ~13 months for ~250bps.

More than anything, the FED will look to limit re-inflation and will keep rates higher to do so…as they did in the mid-90s.

Disclosure: Nothing written here is financial advice or should be used for investment decisions.

Learning Point of the Week:

Where to live?

As you begin your recruiting journey, you’re naturally going to be thinking about where you want to live and what you truly want to do.

This is a discussion about the former, which I think is more critical to happiness than the latter.

Some ‘truths’:

If you go to a T-20 school, it seems like NYC or SF or die (some Boston lifers mixed in)

Bigger cities = more opportunity

Bigger cities = more fun

The reality:

The majority of people you’re close with will either go to NYC or SF and if you don’t live in those cities —you really won’t see those friends that often

There are definitely more junior roles in bigger cities. However, friends working in LCOL cities a). make more on a net basis and b). have less competition for jobs

Your definition of fun should be what you like to do not what everyone else is doing. I personally love outdoor activities and my scope would be super limited if my family wasn’t from the tri-state area allowing for easy access to the ‘burbs

It can be really easy to bandwagon onto the same path as everyone else. But what is right for someone else, may not be right for you. I don’t know a single person who hates where they live and is happy with their life—even if they do something super coveted like mega-fund PE.

NYC and SF are cool places with an abundance of opportunity, but they’re far from perfect. People move in and out of these cities in short duration for a reason. Sure, there is a ton of stuff that you CAN do, but that doesn’t mean your friend group WILL get organized to do it.

Most analysts I know in NYC do the same shit every weekend: hit a local bar in the East Village and drink with your friends from college

Is that really paradise? I don’t think so.

Work where you want to live. Don’t live where you want to work.

Going Forward:

If you run a club, we want to connect with you to partner. Please shoot us an email @[email protected], would love to make your club the most prepared on campus.

Coaching Details:

2 Sessions for $69. (Venmo @ThePulsePrep or Credit Card: $69 for 2 Coaching Sessions)

Pay for 3, get one FREE = $150. (Venmo @ThePulsePrep or Credit Card: (Coaching Bundle $150 for 4 Sessions)

1 hour session = $50. (Venmo @ThePulsePrep or Credit Card: ThePulsePrep—Stripe.com

30-minute session = $30. Venmo @ThePulsePrep or Credit Card: ThePulsePrep—Stripe.com

Email us with your availability and we will be happy to schedule a session @[email protected]

Students we coached for SA 2025 have received offers at Goldman, JP Morgan, Evercore, and many other firms. Roughly 95% of those coached received offers last year!

Please reach out to us with any questions about recruiting or if you’re interested in meeting the team! ([email protected])

We are happy to chat, review resumes, or help set up a coaching session

Proudly Produced,

The Pulse

“The Pulse” #69